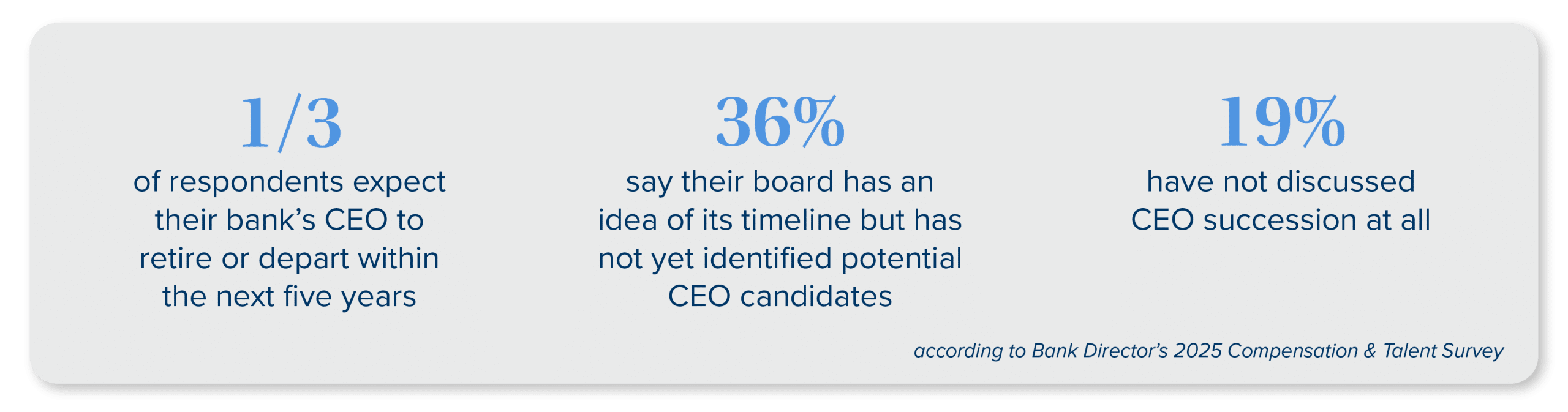

One-third of bank leaders expect their CEO to retire or depart within five years. More than half have either not identified a candidate or not discussed succession at all. That gap, between knowing a transition is coming and being ready for it, is the central problem facing banks and credit unions today, and it is getting harder to ignore as regulatory scrutiny rises and consolidation accelerates.

The numbers come from Bank Director’s 2025 Compensation & Talent Survey, which found that 36% of respondents said their board has a sense of the CEO’s timeline but has not identified potential candidates, while 19% said succession has not been discussed at all.

For many institutions, succession planning still begins too late. Whether it is a CEO announcing retirement, a CRO unexpectedly resigning, or a stakeholder pointing out a leadership gap, the conversation is too often reactive instead of proactive. That timing leaves boards with less room to assess risk, evaluate options, and plan deliberately.

Succession Planning Is Now a Governance and Risk Issue

Traditional succession planning often meant maintaining a list of names, reviewing it annually, and filing it away until the next board cycle. Today, that approach no longer meets the operating realities facing banks and credit unions.

For bank and credit union boards, identifying a successor is only the starting point. Understanding where leadership gaps could create operational, regulatory, or strategic risk is the harder challenge. CEO succession remains a high priority, but the same discipline must extend across all major leadership positions, particularly in functions where specialized expertise is difficult to replace.

Those functions are where the pressure is most acute. BSA/AML, credit, payments, cyber, risk, and technology leadership demand experience that takes years to develop and is increasingly scarce in the open market, and they are also the roles hardest to fill internally. A leader who was effective in a more traditional operating environment may not be equipped for digital transformation, complex compliance expectations, cybersecurity risk, or partnerships with fintech and embedded finance platforms. Modern succession planning means thinking carefully about what each role will demand in two, three, or five years, not just who currently holds it.

Underlying all of this is a demographic reality boards often underestimate: leadership skews more senior, and the pipeline beneath this tier is thinner than it appears. An institution building succession plans around the leadership team it has today, rather than what it will need to be in five years, may not fully appreciate the risk it faces.

In a Consolidating Market, Leadership Risk Becomes Deal Risk

As consolidation accelerates, succession planning has taken on a new dimension: deal readiness. Leadership depth can affect how potential partners, acquirers, or stakeholders assess franchise value, how clients and members respond to uncertainty during integration, and how quickly an institution can stabilize post-close.

Due diligence surfaces tough questions, and the negotiating table is the wrong place to answer them for the first time. Which executives are critical to retain? Where might leadership change be necessary? How will high-potential talent be managed through the transition?

Institutions that have already worked through those questions are in a far stronger position than those that have not.

External Perspective Belongs Earlier in the Process

Internal development efforts are often evaluated against internal benchmarks. Boards, HR leaders, and senior executives may all see progress, but still lack a clear view of how internal successors compare to the external market. Without visibility into comparable talent at peer institutions, fintechs, and other financial services organizations, it is difficult to know whether “ready now” means ready by the standards of the external market, or simply the best option available internally.

Some institutions are now building external benchmarking directly into their succession process. Search firms can also support leadership assessment during acquisitions and integrations, particularly when boards need an outside view of leadership depth, retention risk, or post-close structure.

When brought in early, an executive search firm gives boards and HR a market-grounded view they cannot generate from inside the organization alone. A plan that exists only on paper may not survive scrutiny from stakeholders, regulators, or acquirers.

A Higher Bar for Leadership Readiness

The banks and credit unions best positioned to handle leadership transition will already know where their bench is strong, where it is vulnerable, and how their internal successors compare to the external market. They will have those answers before a vacancy, transaction, regulatory concern, or stakeholder question forces the conversation. Institutions that navigate transitions well are rarely better at finding talent at the last minute. They simply prepared sooner.

Insights in your inbox

Stay up to date on the latest trends and insights shaping the executive search landscape from JM Search’s Blog.